What is a personal loan

A personal loan can be used for various purposes. Including debt consolidation due to unexpected medical care, a new device, on vacation, or even a student loan. You will have to pay it back with interest on a monthly payment over a period of time, usually two to five years.

The interest rate, you pay, are expressed in terms of the annual rate of charge (APR). The average personal loan interest rate was 9.41% in June 2019, however, it may vary from 6% to 36%, depending on your loans, including the analysis, as well as your income, debts, and credit score.

Personal loan does not require any collateral or security, and a minimum amount of paperwork can be achieved. However, as the majority of the loans have to be paid back in a few years.

You can also use it to cover all the costs, including the education, training, wedding, travel, home, home repairs, medical expenses, and even the buying of a gadget. You can use this to help you with the day-to-day expenses in the event of insufficient cash flows.

The loan is divided into two main categories: those that have a banking license and / or the charter, and those who do not. The main difference between these two groups is related to the new regulation.

Banks and credit institutions by the bank of the license, or statute are governed by the Federal Reserve System. Local banks and credit unions are the first thing many people will think of you when you are on a personal loan.

Non-bank financial institutions (NBFI)) – data sources, without a banking license, which is also known as a non-bank financial institution (NBFI) or non-bank financial companies. The main difference is in the terms and conditions of the service as the NBFIs are not allowed to take deposits.

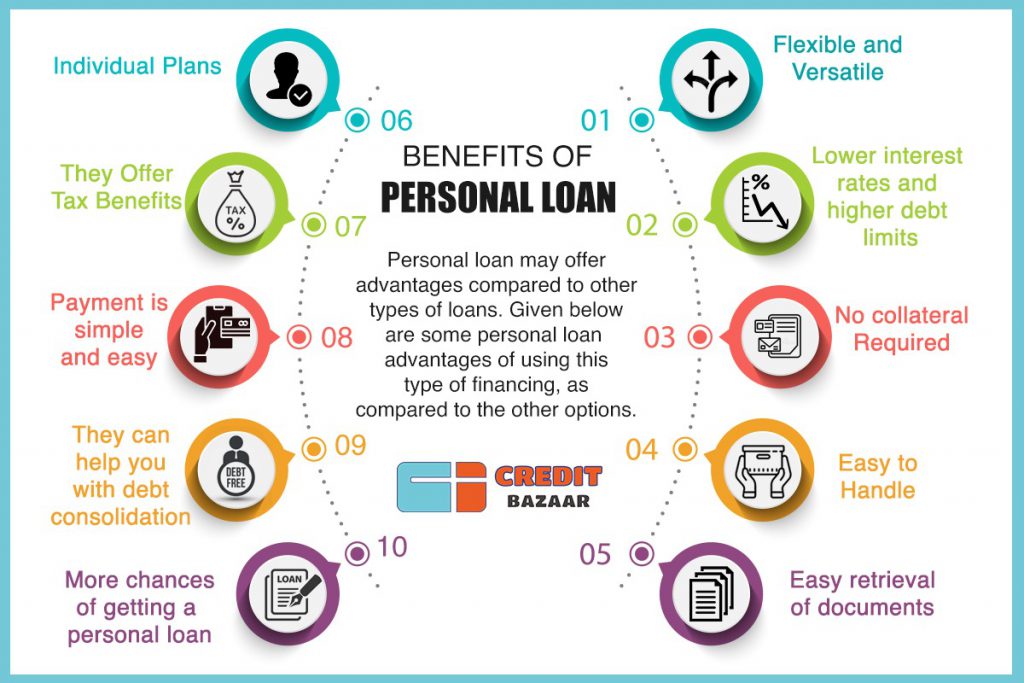

Benefits of personal loan

Personal loan may offer advantages compared to other types of loans. Given below are some personal loan advantages of using this type of financing, as compared to the other options.

1. Flexible and versatile

Some types of debt that can only be used for a particular purpose. For example, if you were to take a car loan, it is the only way to use this money to buy a car. In personal debt, it can be used for many purposes such as, for example, in order to consolidate your debt before paying the medical bills.

2. Lower interest rates and higher debt limits

Consumer loans often have a lower credit card interest rates. In February 2021 at the latest, the average interest rate on a Personal loan was 11.84%, the average interest rate on a credit card was 16.04 per cent. Consumers with a good credit history can qualify for personal loans range from 6 percent to 8 percent.

3. No collateral Required

For unsecured personal loans no collateral is required in order to get the confirmation. This means that you don’t have to show your car, house or other property as a guarantee that you’ll get your money back. If you have the means to pay back the loan as agreed upon by the lender, then you’re going to respond to the significant economic benefits.

4. Easy-to-handle

One of the reasons why some people, use personal loan is to consolidate their debt, and pay the credit card bills using several accounts.. A private loan with a monthly payment of attraction at a fixed rate of interest, easier to manage, more with a credit card, a different interest rate, payment, and other variables.

5. Easy retrieval of documents

The processing is necessary for an individual loan and is less than most other loans. You will need to provide the following personal loan documents in order to qualify for a loan means an identification card, proof of address and proof of income are required.

6. Individual Plans

Instant personal loan are flexible and can be adapted to many needs, like home repairs, vacations, weddings, and medical emergencies. A personal loan can be customized in terms of the rate of interest, repayment period and the expiration of the lease term, depending on the need and ability to pay.

7. They Offer Tax Benefits

Unsecured loans do not guarantee tax savings, you can save your income tax through an individual loan, depending on the purpose for which you will use the resources. If you are using a personal loan to pay for the repairs to the home, purchasing or building a home, or to pay for higher education, you can use the relevant income tax rules in order to get the tax credit.

8. Payment is simple and easy

Paying off a personal loan is hassle-free. A lot of factors, such as, affordable, and simple-to-equity payments, convenient payment options and a stable monthly payment, it tends to be easy. In addition, people have more or less of a good credit score and are able to get a personal line of credit, even if it might be a little higher.

9. They can help you with debt consolidation

If you have multiple debts,interest rate credit card payments, or other secured loan, you can use a personal loan in order to collect all the rest of the debt and clear their portfolio of responsibilities. Consumer loans also offer lower interest rates, more than that of a credit card, then you can use this financial product to share high-interest debt into a low personal loan interest rate. Learn more about personal loans for debt consolidation.

10. More chances of getting a personal loan

In order to offer the consumer a personal loan, in addition to the traditional banking system there are NBFC’s participating as well. This means the greater the opportunity for the client to discover and explore. In addition, in order to improve their performance, NBFC’s provide the consumer with a loan on favorable terms and conditions. Many of the banks lower their personal loan interest rates, also offer lower fines, penalties, etc. Both the NBFS and banks offering personal loans in the range of rs 50,000 up to Rs 15,000.

How to get a personal loan

You are in the bottom of the Rock, the time has come to apply for a loan. If you are planning to apply to different lenders to put together a loan, your application will have been made within 14-30 days. This is known as the prices and a number of questions that will be considered to be as one of to be a lot less of an impact on your credit score.

Your e-mail, indicate which of the additional personal loan documents are required for the application. At first, the collection of these personal loan documents. You will have to submit proof of income (receipt, Form W2), apartment details, official identification cards, and social security number.

The eligibility of the applicant to obtain a personal loan will depend on a number of factors, including a stable monthly income, age, nature of employment, job, CIBIL score, work experience, etc. Your personal information, including the CIBIL score of the pan number and KYC documents.

The eligibility for a personal loan for the self-employed:

Age 22 – 58 year old

The minimum monthly income of at least 15,000

Work experience of at least one year

How to manage your personal loan

1. Creating A Budget

Creating a budget is one of the best things you can do for your financial situation, regardless of their income or debt. Try to manage your personal loan, it is a budget that puts you in a sensual and confusing position that you can always know exactly where your money is going and how much is in it. If you are afraid to check into a bank account and you are not sure where you’re overspending, and it’s getting difficult to keep a track of your payments then set up a budget, that is your solution!

2. Make On-Time Payments

Make monthly payments on time, it is the best way to avoid late payments and penalties, monthly payments take up a lot of consideration in your credit score. This is overkill, and very often, the results of which will work with your financial situation, so keep them in mind and do everything you can in order to stay on top of payments.

When you create a budget, you come to realize that it’s more easy to make payments on time. Budget is like a business plan for the portion of the money set aside each month for your payments. You will not miss any payments on your loan through budgeting.

3. To Pay More Than Your Minimum

The same strategy is at the beginning of the down payment, it will help you to spend more in months, at least when you can. By paying a little more each month, you are ahead of the loan, as well as some other economic benefits.

First, making additional payments on your loan will reduce the total amount of time of your payment. This is going to help you stay on top of both the debt and repairs and your financial independence in order to stay ahead of its time, true to the line of credit, you will reduce the amount of interest that you will need in order to save you money in the long run.

4. Consolidate Your Loans

For customers who manage a lot of personal loans, consolidation can be a great way of simplifying the pay down of the debt. Debt consolidation is when you take out a large loan, which can be used to pay off other loans. So, instead of having to make monthly payments to several lenders at different rates and requirements, you can make a single payment.

Debt consolidation is especially useful if you are able to secure a low personal loan interest rate on your new loan that is lower than the average of the interest rates on your current loans.

5. Stay Up-To-Date With All Your Credit Score

Finally, keep an eye on your credit score when you pay for a single credit. Your credit score plays a huge role in your performance, and it is an important link, in order to qualify for a loan, your credit score will also affect your personal loan and it’s interest rates.

To manage your personal loan and your credit score be true to your monthly plan at the time, and not be behind in any of your monthly payments which will put your score down, you will improve your credit score by maintaining a steady balance. On the other hand, the backlog of payments is low, your credit score will also be.

6. Please Read The Terms And Conditions:

Probably nothing is more important than the beautiful font before deciding on a personal loan. Check out the most important details, such as the schedule, the maximum loan in a timely manner, all the criteria that killed terms of the amount of time it takes to get your loan has been confirmed.

Also, please make a payment for the recovery. Some loans offer very low personal loan interest rates, which is a part of the third-party campaign, but this is compensated for by the high tariffs.

How we can help you to get a personal loan?

Thanks to technology, it is now possible to apply for a private loan on the net, and it is pretty much easy and fast. There are a variety of online platforms, which provide a simple system in order to apply for a loan. You can use the Credit Bazaar website in order to apply for an online personal loan in just a few simple steps. Here’s a quick guide to getting a personal loan on the web.

Please visit the Credit Bazaar, please go to the Credit line, click on the personal loans of Loans section, and you will be taken to the next page.

On this page, you will need to provide your basic personal information, including your name, contact details, address, etc., Here, you will also need to provide details of the desired loan amount, repayment period, your monthly income and other payments relating to the payment of which is being done for the time being. You will also be required to provide details of your previous score if you don’t take it out on them. Now click the Submit button.

After that, you will have to go to the next page. Here, you will see a detailed comparison of the loans denominated in a variety of lenders. Here, you will need to carefully consider the various options that are available, and some important parameters such as grade, quotes, payment, etc. etc., to choose what is best according to your needs.